Safeguarding Your Identity: Essential Tips for Financial Security

Statistics show that nearly 33% of Americans have faced some identity theft attempts in their lives, and experts estimate there is a new case of identity theft every 22 seconds. As financial professionals, one of our primary goals is to help our clients create a financial strategy and protect their wealth. In today’s digital age, identity theft threatens your finances, so it’s crucial to understand the risks and take proactive measures.1

This blog aims to equip you with practical strategies for protecting your personal and financial information with the goal of maintaining your financial well-being.

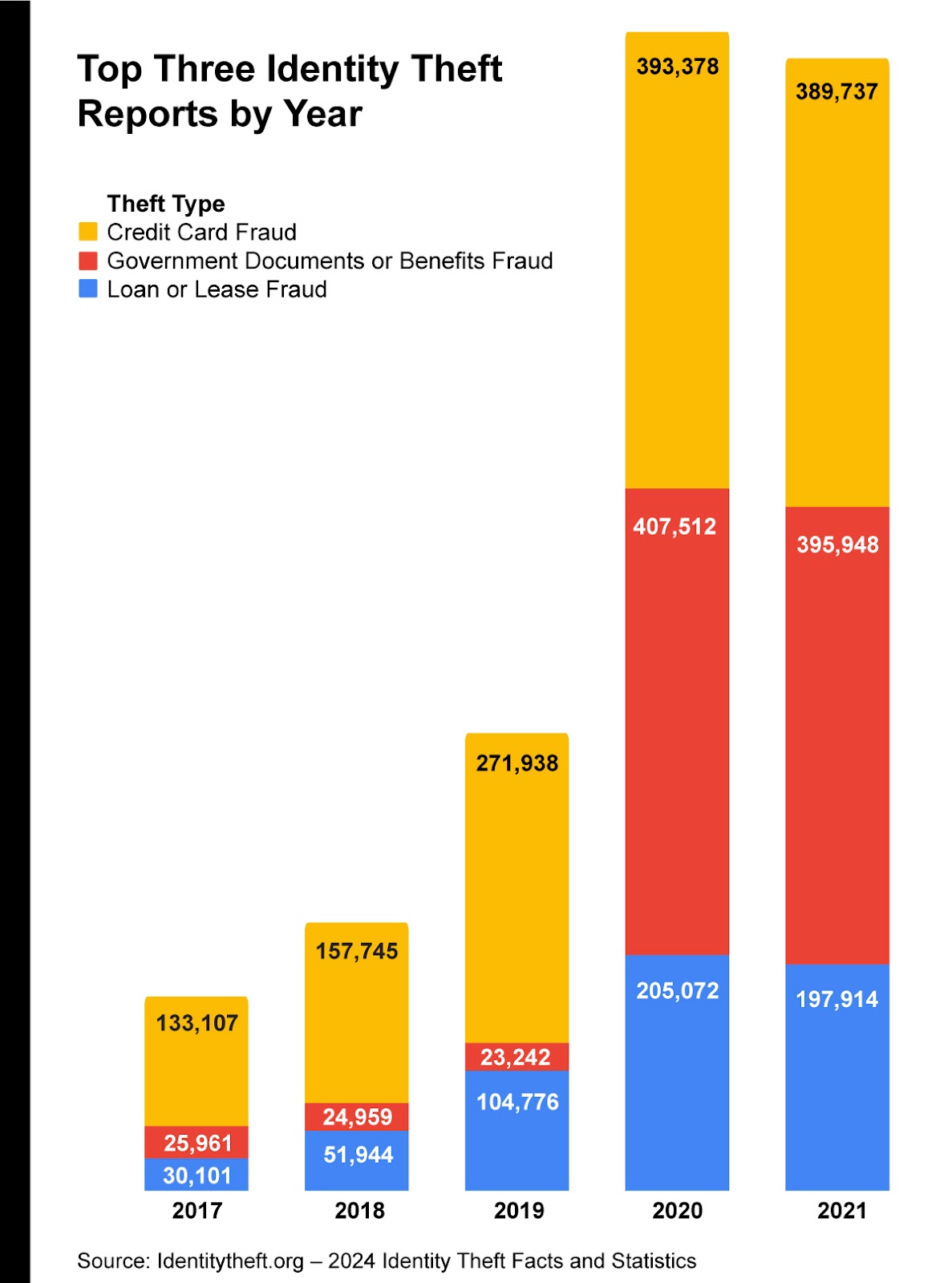

The most common types of identity theft are1:

- Credit card fraud

- Government documents or benefits fraud

- Loan or lease fraud

Financial Implications of Identity Theft

The financial hardships caused by identity theft can last for months or even years after your personal information is exposed. Depending on the type of data identity thieves obtain, the recovery process can involve several hurdles. Victims often need to dispute fraudulent activities in their credit files and work to restore their good credit. This may include cleaning up and making changes to compromised bank accounts.2

If an identity thief uses your Social Security number to obtain employment, you may need to work with the Social Security Administration. Similarly, if you become a victim of tax refund identity theft or an identity thief's income makes it appear you are under-reporting your income, you may need to work with the IRS.2

This blog is for informational purposes only and is not a replacement for real-life advice. We encourage you to consult your tax, legal, and accounting professionals if you believe identity theft involves using your tax records.2

Identity theft involving sensitive, personally identifiable information like your Social Security number can have long-lasting effects. Thieves may wait months or even years to use your information, or they might sell it on the dark web, requiring you to stay vigilant indefinitely. Legal fees and other costs could add to the financial impact if your identity theft issue is complex. Some victims even need to seek government assistance during recovery, highlighting the potential magnitude of identity theft hardships.2

Common Sense Protections

It can be difficult for victims to deal with identity security issues because bad actors are becoming more sophisticated all the time. You can use technology-enabled safeguards to help protect your identity and personal data, such as antivirus protection software, password managers, identity theft protection, virtual personal networks, and two-factor authentication on devices and accounts. There are also other actions you can take to help manage the risk of becoming a victim, including:

- Don’t let your mail sit uncollected too long.

A low-tech way criminals can steal your identity is to simply take bank or credit card statements, utility bills, health care or tax forms, or pre-approved credit card offers out of your mailbox. So, don’t let your mail sit uncollected too long. Also, if you are going away, have a trusted neighbor bring in your mail or put your mail on hold with the post office.3

- Review credit card and bank statements.

By reviewing your credit card and bank statements, you may be able to spot any suspicious activity. Thieves with your credit card number or bank account information could make small purchases to see if they can get away with it. These transactions can go unnoticed. Thieves may try to make large purchases if they get away with minor ones.3

- Freeze your credit

In some cases, you may want to consider freezing your credit file so no one can look at or request your credit report. That means no one can open an account, apply for a loan, or get a new credit card while your credit is frozen. Remember, a credit freeze applies to you as well. To get started, contact each of the three major credit reporting agencies. In some instances, credit freezes are free and won’t impact your credit score.3

- Create different passwords for your accounts.

According to the Federal Trade Commission (FTC), secure passwords are longer, more complex, and unique. Many people use the same password for multiple accounts, which could be problematic. You should consider creating different passwords for various accounts and avoid using information related to your identity, such as the last four digits of your Social Security number, your birthday, your initials, or parts of your name.3

The FBI and the National Institute of Standards and Technology have issued guidelines stating that passwords should consist of at least 15 characters because these are more difficult for a computer program or hacker to crack. Regarding security questions, the FTC’s guidelines suggest questions that only you can answer; avoid information that could be available online, such as your ZIP code, city of birth, or mother’s maiden name.3

- Consider shredding documents with personal information.

As stated earlier, not all identity theft is high-tech. Old-fashioned dumpster diving might sound like a thing of the past, but it still happens. Consider buying a household shredder and destroying sensitive paperwork, such as credit card and bank statements, utility bills, and other documents containing personally identifiable information.3

- Opt out of prescreened credit card offers

Credit card companies often send prescreened offers to open new accounts, and criminals can intercept these mailed or emailed offers and open accounts in your name. One way to help avoid a potential identity theft issue is to opt out of receiving these offers.2

- Clean out your wallet4

Here are a few suggestions:

- Social Security number

Leave your Social Security card at home in a safe location. Those nine digits can help an identity thief to obtain loans or credit card accounts in your name. A bad actor could also use your Social Security number with the IRS.

- Checks

Consider leaving checks and deposit slips at home. These items may contain more information than you think, including your name, address, bank name, routing number, and account number.

- Password cheat sheets

Scraps of paper with sensitive information, such as PINs and passwords, can be risky, so add them to the list of what not to keep in your wallet.

- Numerous cards

It may be best to limit the number of credit cards in your wallet. The same goes for excess cash and gift cards.

- Bypass the PIN at the gas pump5

One of the most common schemes is when criminals install a skimming device directly over the credit card slot at a gas pump. These skimmers capture and store your card data when you insert or swipe your card. If something looks off, don’t use that pump. Also, if you use a debit card to pay for your gas, bypass the PIN if possible and use your zip code instead. That may prevent someone from stealing your PIN using a pinhole camera.

Safe Disposal of Digital Devices

Improper disposal of old digital devices is a key but often overlooked aspect of identity theft. Simply deleting files may not be enough on some digital devices, as thieves may be able to recover the data. Therefore, safe disposal is critical. Many communities have secure electronics recycling events where devices can be disposed of. However, it’s important to note that different devices and storage media types may require different disposal methods.

Identity Theft Protection Services

Identity theft protection services offer a range of features designed to detect identity theft, alert you to identity theft, and help you recover from identity theft. These services typically monitor credit reports, dark web activity, and public records for signs of fraudulent use of personal information. When suspicious activity is detected, they alert the user and provide next steps. While these services can be helpful, their effectiveness can vary. However, these services can be a valuable first step for those who lack the time or expertise to monitor their credit and personal information.

What to Do if Your Identity Has Been Stolen

You may not know that you have been a victim of identity theft immediately when it happens, but there are warning signs you can look out for, such as:6

- Bills for items you did not buy

- Debt collection calls for accounts you did not open

- Information on your credit report for accounts you did not open

- Denials of loan applications

- Mail stops coming to or is missing from your mailbox

If you are a victim of identity theft, you may want to place fraud alerts or security freezes on your credit reports. A fraud alert requires creditors to verify your identity before opening a new account, issuing an additional card, or increasing the credit limit on an existing account based on a consumer's request.

Pro tip: When you place a fraud alert on your credit report at one of the nationwide credit reporting companies, it must notify the others.7

Protecting your identity is an integral part of maintaining your overall financial health. As financial professionals, we believe safeguarding your personal information can be as crucial as making sound investment decisions. By implementing these preventive measures and staying vigilant, you can help manage the risk of becoming a victim of identity theft. Remember, your financial security encompasses every aspect of your financial life.

If you have any concerns about identity theft or would like to discuss how it fits into your broader financial strategy, don’t hesitate to contact us. We’re here to help provide you with information that can help improve your personal finances.

Sources:

1. IdentityTheft.org, 2024

https://identitytheft.org/statistics/

2. Lifelock.Norton.com, February 4, 2021

https://lifelock.norton.com/learn/identity-theft-resources/lasting-effects-of-identity-theft

3. U.S. News & World Report, May 4, 2024

https://www.usnews.com/360-reviews/privacy/identity-theft-protection/10-ways-to-prevent-identity-theft

4. Discover, May 23, 2023

https://www.discover.com/online-banking/banking-topics/7-things-you-should-never-carry-in-your-wallet/

6. USAGove.com, July 28, 2024

https://www.usa.gov/identity-theft#:~:text=Identity%20theft%20happens

7. Consumer Financial Protection Board, February 27, 2024

https://www.consumerfinance.gov/ask-cfpb/what-do-i-do-if-i-think-i-have-been-a-victim-of-identity-theft-en-31/

WANT TO RECEIVE UPDATES TO YOUR INBOX?

Sign up for our newsletter