10 Facts You May Not Know About Social Security

Social Security is often misunderstood or underestimated in retirement strategy. However, as financial professionals, we've seen how it can play a crucial role in our clients' overall financial strategy, regardless of their income level or net worth.

This program extends beyond basic retirement benefits, offering vital programs and strategic opportunities that can influence your financial future. From unexpected benefits to strategic claiming decisions, understanding the nuances of Social Security can lead to more informed financial choices.

The following ten surprising facts about Social Security reveal critical insights that may be able to enhance your retirement strategy. These lesser-known aspects demonstrate why Social Security deserves careful consideration in any comprehensive financial strategy, no matter your current financial status.

1. Social Security is more than just retirement benefits

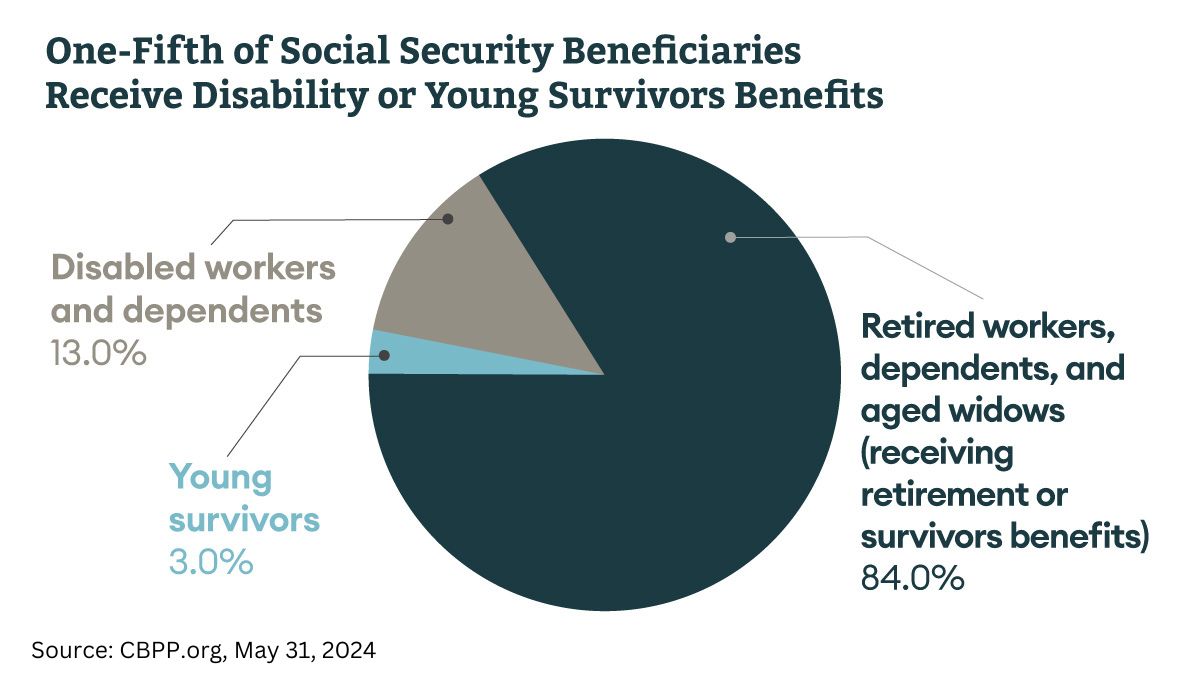

Many people primarily view Social Security as a retirement program, but it also offers critical financial support in the event of death or disability.

According to the Social Security Administration, approximately 96% of people aged 20-49 who worked in jobs covered by Social Security in 2023 had access to these protections. For a young worker with average earnings, a spouse, and two children, that's equivalent to a life insurance policy with a face value of nearly $948,000 in 2023.1

What’s more, about 90% of people aged 21-64 who worked in covered employment in 2023 were insured through Social Security in case of severe disability. While it is not something we like to think about, 8% of recent entrants to the labor force will die before reaching the full retirement age, and many more will become disabled, making Social Security a vital safety net.1

2. Delayed claiming can increase benefits

As stated by the Social Security Administration, for each year you delay claiming Social Security past your full retirement age (FRA), your benefits increase by 8% until age 70. This strategy can potentially benefit individuals who can afford to delay claiming their benefits.2

While waiting to take your benefits may sound like an easy answer, deciding when to begin taking Social Security is one of our most common questions. It may seem straightforward, but it’s more complex than it looks. Since everyone’s circumstances are unique, there are a few considerations that you may want to take into account:

- Will you continue working? Social Security may withhold some of your payment if you work while collecting early benefits.

- Are you married, and does your spouse anticipate benefits?

- How is your health? Your health status could affect your decision on when to start taking benefits.

Your answers to these questions can significantly impact your Social Security strategy.

3. Social Security benefits are adjusted for inflation

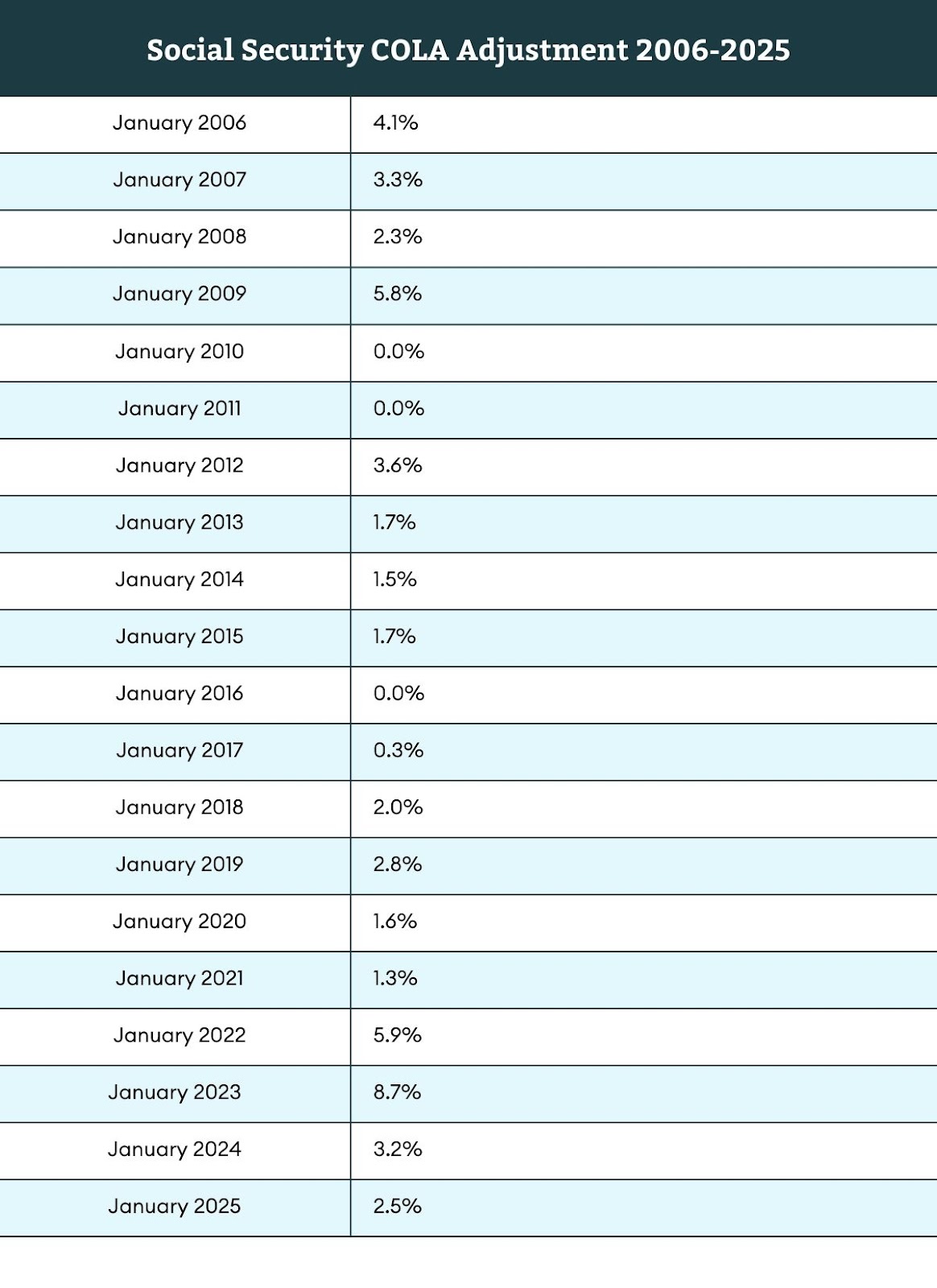

Unlike some private pensions, Social Security benefits can be adjusted annually for inflation. This Cost-of-Living Adjustment (COLA) is designed to help maintain the purchasing power of your benefits over time, potentially managing the impact of inflation in retirement. According to the Social Security Administration, the COLA for 2025 is 2.5%. This follows an 8.7% COLA for 2023, one of the most significant increases in recent history due to high inflation the year before. Note that there is not always a COLA increase every year. As the chart shows, there were three times in the past 20 years when beneficiaries received no COLA due to a lack of inflation.3

4. Benefits may be subject to taxation

Many retirees are surprised that their Social Security benefits may be subject to federal income tax. This taxation can affect your overall retirement income strategy. Here's what you need to know:

Taxation Thresholds:4

- Taxation begins when your "combined income" exceeds certain thresholds:

- $25,000 for individuals

- $32,000 for married couples filing jointly

- Your combined income is the sum of:

- Your adjusted gross income

- Nontaxable interest

- Half of your Social Security benefits

- If your combined income exceeds $34,000 (individual) or $44,000 (married filing jointly), up to 85% of your benefits may be taxable.

Managing Tax Payments:4

If you owe taxes on your Social Security benefits, you have two choices:

- Pay the IRS directly when you file your annual tax return.

- Have taxes withheld from your monthly Social Security payment.

- You can choose to have 7%, 10%, 12%, or 22% of your monthly payment withheld for taxes.

State Taxation:

While most states don't tax Social Security benefits, the states that still do, according to an August 2024 report in Kiplinger.com, include Colorado, Connecticut, Minnesota, Montana, New Mexico, Rhode Island, Utah, and Vermont. Each state has its own rules and exemptions.

Strategic Considerations:

- The taxation of Social Security benefits can affect your overall retirement income strategy.

- Consider how other sources of retirement income might push you into a higher taxation bracket for your Social Security benefits.

- Roth IRA distributions are not included in the combined income calculation, potentially making them a valuable tool in managing your tax liability.

- To qualify for the tax-free and penalty-free withdrawal of earnings, Roth IRA distributions must meet a 5-year holding requirement and occur after age 59½. Tax-free and penalty-free withdrawals can also be taken under certain other circumstances, such as the owner's death. The original Roth IRA owner is not required to take minimum annual withdrawals.

By working with financial and tax professionals, you may be able to develop a strategy that is designed to manage your tax burden while maximizing your retirement income.

5. Spousal benefits can enhance retirement income

Your non-working spouse may be eligible to collect Social Security benefits based on your work record. To qualify for spousal benefits, you must be collecting Social Security retirement or disability benefits, and your non-working spouse must:

- Be at least 62 years old (Any age if you have a child who is younger than 16 in your care or has a disability and is entitled to benefits on your spouse’s record.).

- Be married to you for at least one year.

The maximum spousal benefit is 50% of your full retirement age benefit amount. Social Security will permanently reduce benefits if your spouse claims before their full retirement age. If you delay claiming past full retirement age, the spousal benefit does not increase beyond 50%.5

In the event of your death, your spouse may be eligible for survivor benefits based on your Social Security record but will not receive your benefits in addition to their own—they'll only receive whichever benefit is higher. If your surviving spouse, or a surviving divorced spouse, remarries before they reach age 60, they cannot receive benefits as a surviving spouse while married. If your surviving spouse, or a surviving divorced spouse, remarries after they reach age 60, they will continue to qualify for benefits on your Social Security record.6

6. Social Security may act as a buffer against market volatility

Because it provides stable income, Social Security offers a steady income stream that is not dependent on market performance. This monthly payment can help cover basic living expenses without tapping into investment accounts during market downturns.

7. Your total benefit might surprise you

You might be surprised by the aggregate Social Security benefit you may be entitled to. The expected value of lifetime Social Security benefits for a single male with maximum taxable earnings ($160,200 in 2023 dollars) who turns 65 in 2025 is $39,800 annually and $634,000 over an average lifespan. For a married one-earner couple with maximum taxable earnings, the benefit would be $59,600 annually starting in 2025 and $1,076,000 total based on life expectancy.7

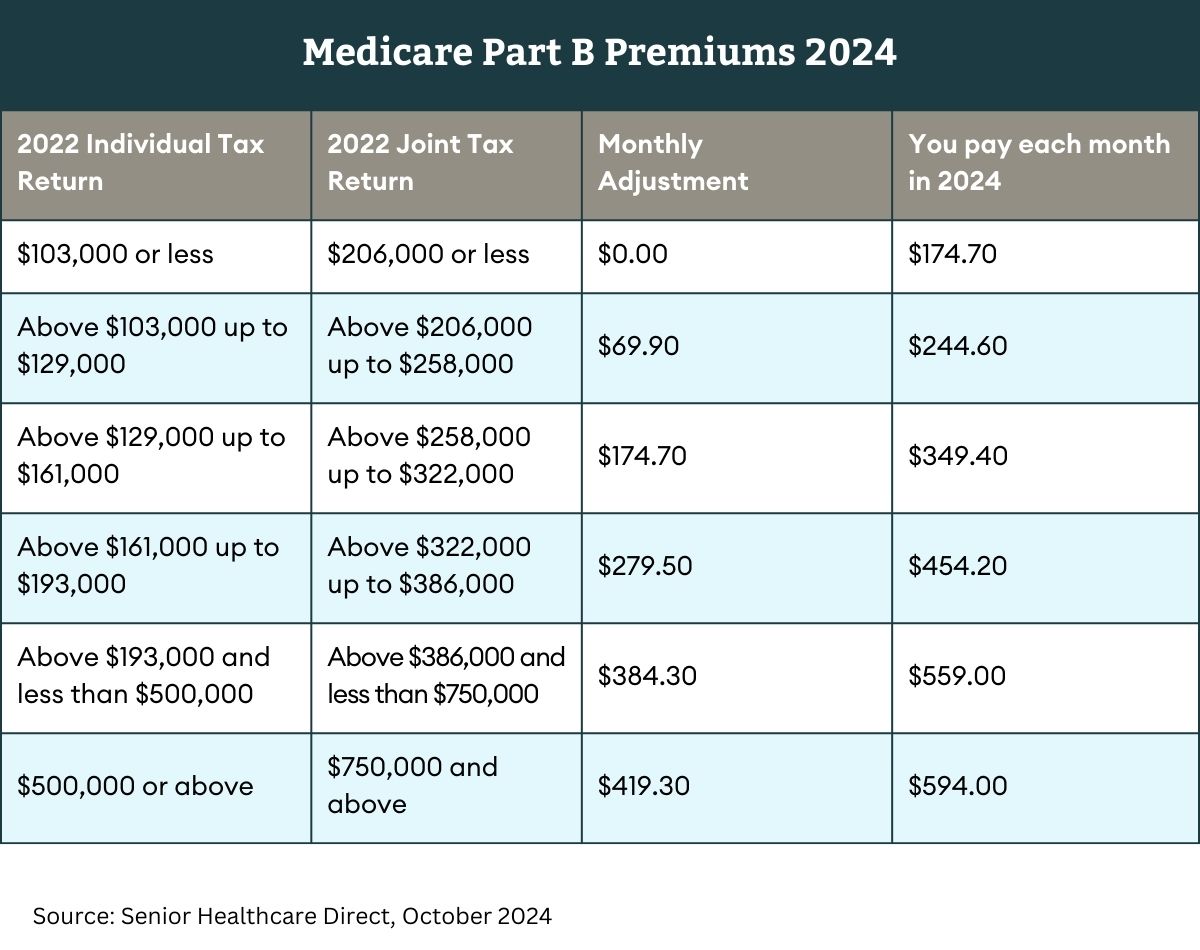

8. Higher income can mean higher Medicare premiums

You may not be aware that high-income beneficiaries may pay higher premiums for Medicare Part B and Part D. In 2024, individuals with modified adjusted gross income above $103,000 (or $206,000 for married couples) will pay higher premiums. The chart below details the increased monthly costs for Medicare Part B based on income levels.8

9. Social Security offers international benefits

If you're considering retiring abroad, it's essential to know that Social Security benefits can generally be received while living in most foreign countries. This income can provide flexibility in retirement living arrangements. Once you begin receiving Social Security benefits abroad, the Social Security Administration will send you a questionnaire every one to two years. This questionnaire will determine if you are still eligible for benefits. If you do not respond, your benefit payments may be stopped.9

While Social Security payments can often continue if you are living abroad, Medicare won't pay for health care or supplies you get outside the U.S. Some exceptions would allow you to get coverage outside the U.S. under Medicare Part A (Hospital Insurance) and Part B (Medical Insurance).10 So, if you plan to be an ex-pat upon retirement, please speak to a professional about your plans and do your research.

10. The Windfall Elimination Provision may affect benefits

According to the Social Security Administration, individuals who have worked in jobs not covered by Social Security (such as some government positions) and are eligible for a pension from that work may see their Social Security benefits reduced due to the Windfall Elimination Provision. Understanding if this provision applies to you is crucial to accurately determining how much Social Security benefits you can expect.

Don’t underestimate the importance of Social Security

While Social Security may not be the primary source of retirement income for many individuals, it can play a significant role in a comprehensive retirement strategy. Understanding these lesser-known aspects of Social Security can help you make more informed decisions about your retirement and potentially enhance your overall financial picture.

As financial professionals, determining your sources of retirement income and how your different sources can work best together is an integral part of our services. If you have any questions about retirement income, including Social Security, please do not hesitate to contact our office.

Sources:

1. Center on Budget and Policy Priorities, May 31, 2024

2. Social Security Administration, October 2024

3. Social Security Administration, October 2024

4. Social Security Administration, October 2024. This blog is for informational purposes only and is not a replacement for real-life advice. Consult your tax, legal, and accounting professionals before modifying your Social Security strategy.

5. Social Security Matters, July 15, 2024

6. Social Security Administration, October 2024

7. Urban Institute, July 2023

8. Senior Healthcare Direct, October 2024

9. USA.gov, October 2024

10. Medicare.gov, October 2024

WANT TO RECEIVE UPDATES TO YOUR INBOX?

Sign up for our newsletter